3/3/2020

We all know who’s going to foot the bill. Hint: it’s not billionaires

February 24, 2020

Under the plan, Sanders plans to provide universal child care and pre-K, spending $1.5 trillion over a decade for the “free” program. All Americans would guaranteed child care through age 3 followed by free pre-kindergarten education.

“As president, we will guarantee free, universal childcare and pre-kindergarten to every child in America to help level the playing field, create new and good jobs, and enable parents to more easily balance the demands of work and home,” Sanders said in a statement.

Sanders says he would fund the program through his “tax on extreme wealth” over $32 million. His campaign claims that tax would bring in some $4.3 trillion over 10 years.

The socialist has a slew of “free” programs that cost trillions. He supports a single-payer “Medicare for All” system, wants to cancel all student debt and make public college free, and raise the minimum wage to $15 per hour. And Sanders advocates providing free breakfast, lunch and dinner to all students, regardless of income level.

“Exact cost projections on all of Sanders’ proposals aren’t available, in part because he hasn’t fully fleshed out some of the ideas he’s embraced (such as universal pre-K and child care),” CNN reported in January.

But a wide variety of estimates put the likely cost of the single-payer health care plan he has endorsed around $30 trillion or more over the next decade. Depending on the estimates used, including projections from his own campaign, the other elements of the Sanders agenda — ranging from his “Green New Deal” to the cancellation of all student debt to a guaranteed federal jobs program that has received almost no scrutiny — could cost about as much, or even more than, the single-payer plan. That would potentially bring his 10-year total for new spending to around $60 trillion, or more. …

“I think if the price tag for the Sanders agenda was [better] known … voters would blanch — even Democratic primary voters would blanch,” said Jim Kessler, executive vice president for policy at Third Way, a centrist Democratic group. “The truth of the matter is in primary elections both in 2016 and so far in this one, he’s allowed to skate. He gets graded on a curve. But if he were the nominee, the curve is over. The Republicans will spend a billion dollars picking apart every one of his plans.” …

The sheer size of Sanders’ spending agenda dwarfs the proposed tax increases he has offered to pay for it, economists across the ideological spectrum agree. Brian Riedl, a former Senate Republican budget aide who’s now a senior fellow at the conservative Manhattan Institute, has calculated that at most Sanders’ existing proposals to raise taxes on the wealthy, Wall Street and corporations would raise about $23 trillion over the next decade.

“There is nowhere near enough resources that you can credibly collect to pay for spending of this size [from the rich],” agrees MacGuineas. “When you are talking about a doubling in the size of the government, you are talking about significant tax increases on the middle class.”

In addition, Sanders supports a plan offered by Rep. Alexandria Ocasio-Cortez she has dubbed the “Green New Deal.” The cost for that program: $93 trillion.

Published on May 5, 2019

By MATT WALSH

I have discovered, much to my shock, that it is quite unpleasant to be in debt. I have to make payments every month, according to the agreement that I knowingly and purposefully signed. Apparently, the lender really wants the money back. I thought maybe they were joking or being sarcastic when they sat me down and said: “This is how much you will owe and this is what your monthly payments will be.” I could have sworn I saw the guy wink, as if to say, “This is all a formality — you don’t really have to make good on the loan. Have fun and don’t worry about it.” Now I suspect that maybe his eye was just twitching from some sort of nerve damage.

Here I am, then, with the debt I agreed to take on for the sake of the product I intentionally purchased. But the financial obligation is hard. It makes my life difficult. I wake up in cold sweats wondering how this happened to me. Well, practically speaking, I know how it happened. I went and took out a loan and now I have to pay it back. Look deeper, though, and you’ll discover that it’s not my fault. I am the victim here.

First of all, you need a car in this day and age. I had no choice but to buy one. Sure, some people get by without cars. It’s technically possible to survive without a car. For a while, anyway, until you die from exhaustion, or hypothermia, or you get eaten by wolves or whatever, because you have to walk everywhere. The point is, I’m not going to be some plebe wandering down the sidewalk. That lifestyle might work for some people — less interesting, less important people — but not me. I’m me, after all, for God’s sake.

Now, you might argue that I could have easily purchased an affordable vehicle. I didn’t have to spend six figures on a car when there are thousands of different options and many of those options wouldn’t result in a mountain of debt. I could have bought a really cheap used vehicle, driven it around for a while, and then eventually traded it for a nicer model once I had the money and means to afford it. Or I could have consigned myself to the miserable life of a pedestrian for a period of time — a few years, at most — while I earned a living, saved money, and put myself in a better position to purchase a quality automobile. There are many things I could have done, you might say. But that’s because you don’t understand.

I needed the nicest car, right away, immediately, no matter the cost. Those “responsible” plans you mention might work for other people, but, like I’ve already explained, I’m not other people. I’m a special case. There are certain things life owes me: Status, popularity, luxury, Lamborghinis. Don’t you see how this works? It is not the lender who is owed. Rather, I am the one who is owed. So, I did what was right for me. Even if it wasn’t right for me. You are not entitled to any more of an explanation. You should be satisifed with that. Why are we even talking about you, anyway? This is about me, remember? Let’s not lose sight of the real issue.

I propose — no, I demand — Lamborghini loan forgiveness. It is simply unfair that I have saddled myself with this unspeakable financial burden. It is the worst injustice I have ever perpetrated against myself, and I demand restitution. I don’t really care how the matter is resolved, just as long as it ends with me cruising debt-free down the highway in my bright yellow Lambo. Yes, I will be keeping the car. I’m not asking for a refund here — I’m talking about forgiveness. The debt should be wiped clean. Like it never happened. Poof. Gone.

Who is going to pay back the lender? Again, not my concern. If, for some reason, restitution is necessary, then take the money from my neighbor. He paid off the loan on his Honda Civic years ago. He’s got plenty of extra money lying around, I’m sure. It is perfectly just to force someone else to assume my financial responsibilities. I remind you for the umpteenth time: This is me we’re talking about. I would never want to force my neighbor to pay off some random rube’s car, or boat, or patio, or whatever. That would be totally immoral. It would be stealing. It’s unthinkable. But I’m not a random rube. I’m special. I’m important. I have a Lamborghini. Now someone just needs to pay for it.

By Mac Slavo

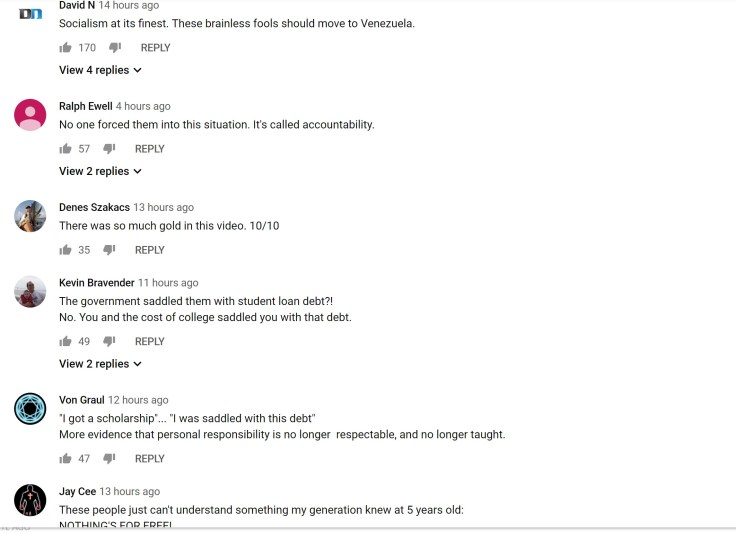

According to The Institute for College Access and Success (TICAS) Project on Student Debt, the average borrower will graduate with $26,600 in student loan debt. That means, that before a dollar is made using the degree, most Americans will owe money to someone else. The trend is not doing the economy any favors either. One in 10 graduates will accumulate more than $40,000 in debt and 1% of graduates will accumulate over $100,000 in student loan debt.

According to the Consumer Financial Protection Bureau, student loan debt has reached a new milestone, crossing the $1.2 trillion mark — $1 trillion of that in federal student loan debt in 2013. That debt currently stands at a whopping $1.5 trillion. And according to a report by Forbes, this is a negative sum game for both the borrowers and the economy. Although taking out massive amounts of debt for college is now the new normal, it’s crippling the economy and the personal financial situations of millions of borrowers.

However, the Pittsburg Post-Gazette says there isn’t a student loan crisis in a recent op-ed. But this information is coming from those who profit off of student loans, such as college presidents. But others say that this is simply a matter of supply and demand and there is more demand than supply. Additional options should be presented to those who have become intent on debt rather than a mandated degree. Educating students on the power of debt should also be considered to help stave off and eventually eliminate this problem.

“There has been a big shift in terms of who should bear the burden of the cost of education,” said Benjamin Keys, a Wharton real estate professor with a specialty in household finance and debt. “We know the stories of our parents, that they could earn enough working as a lifeguard in the summer to pay for a semester of college. The growth of tuition costs relative to teen wages — indeed, all wages — has veered sharply upwards.”

“We’ve come to a place where most students have to borrow in order to pay the cost of completing a bachelor’s degree,” said University of Pennsylvania professor Laura W. Perna, executive director of Penn’s Alliance for Higher Education and Democracy.

Of course, that’s little consolation to those who cannot pay for the degree they went into debt to finance. The student loan dynamic is without a doubt changing the culture of the country. People no longer view debt as something they need to avoid to eliminate slavery to the lender, but something as “necessary” to get ahead. Perhaps this is also why people cannot imagine their life without enslavement to the government. They have been conditioned to believe this is “normal.”